Building the Energy Future While the Rest of America Argues About It: America’s Energy Belt

Startup ecosystems do not happen at the city level, no matter how many branding exercises a mayor commissions or how many innovation districts get ribbon-cut in the same news cycle. They happen at the regional level, with sector specialization that compounds across geography where varied strengths and weaknesses are found throughout; the people writing the checks, the policies, and the press releases keep getting this backward.

Cities compete for what regions actually produce. Until economic development professionals internalize that, the United States leaves opportunity on the table; instead, funding hundreds of small, redundant, undifferentiated programs while the entrepreneurs and innovation need sector specialization far more than local support.

An extensive part of the book Startup Ecosystems, and the single point that economic development teams in Albuquerque, Phoenix, Houston, Tulsa, Little Rock, and every smaller town between them most need to absorb is that ecosystems are not built around tech in the abstract. They are built around what a region already does at industrial scale, with anchor employers that make founder risk survivable, and with a supply chain of capital, customers, and talent that is sector-specific rather than generic. A SaaS founder in Austin and a biotech founder in Houston do not share the same ecosystem; they share a state. The “Texas ecosystem” is a marketing artifact. The Houston petrochemical engineering complex, the West Texas oil and gas basin, the North Texas defense and aviation manufacturing cluster, and the Austin startup scene are different ecosystems whose only meaningful overlap is geography and tax policy. I covered the regional version of this for aerospace in The Texas Aerospace Space; I want to apply the same logic now where it matters even more today, to energy.

The Energy Demand Shock Nobody Is Considering Honestly

The United States is in the early innings of an energy demand shock that nothing in policy or planning has really prepared the country for evident in the politics ongoing. Regions of the world that are going to win are not the ones debating whether AI is overhyped, whether net-zero pledges are realistic, or how many data centers we need, they are the ones with the energy startups and innovation, building and optimizing generation, transmission, storage, and grid software at the same time the demand is arriving. Texas Standard from Moody College of Communication, reported that Texas is expected to see its peak electricity demand increase by more than 60% in the next five years, which is why many of the largest AI infrastructure companies are now investing in their own energy infrastructure. The Stargate flagship in Abilene alone is on track to draw 1.2 gigawatts of electrical capacity once fully outfitted, enough to support the load of roughly 750,000 homes. Crusoe CEO Chase Lochmiller described the broader build-out, in a Bloomberg tour covered by R&D World, as “the largest capital investment in infrastructure in human history.”

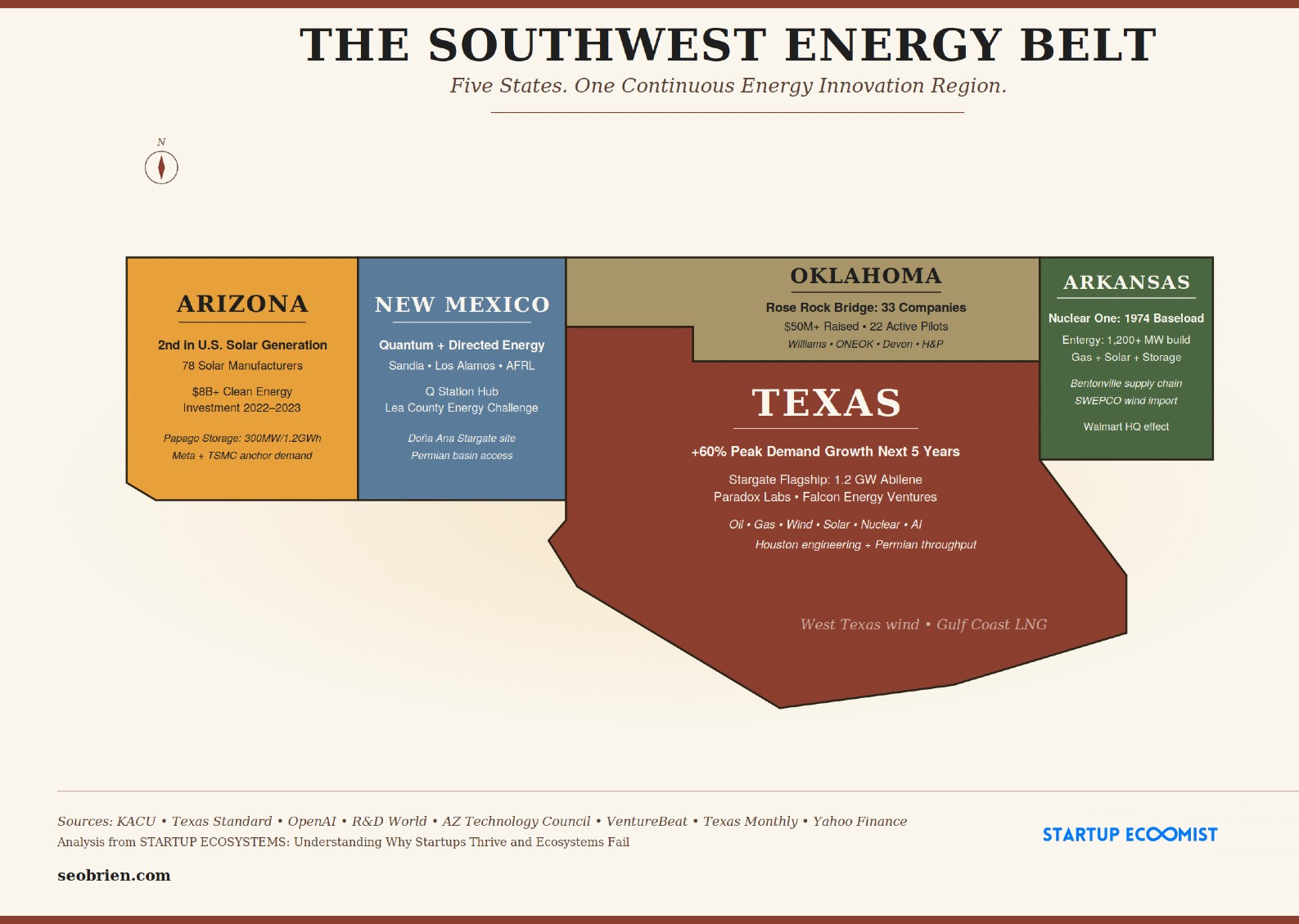

Quantum computing, hyperscale data, aerospace propulsion testing, and industrial robotics are all energy-intensive sectors whose growth assumes a grid that nobody has actually committed to building. The country can keep arguing about energy production of the past, or it can finance and engineer the energy production of the future. The region that is actually doing the latter, while everyone else hosts panels about it, is the Southwest; specifically, New Mexico, Arizona, Texas, Oklahoma, and Arkansas. Five states, one continuous region, one labor market, one developing capital pool, and absolutely no coordinated narrative tying them together.

That last part is why I write: the opportunity.

The Southwest is Building the America’s Energy Belt While the World Argues Over It

NEW MEXICO HAS BEEN BUILDING THIS FOR EIGHTY YEARS

New Mexico is the state that the rest of the country has been undercounting since the Manhattan Project. I argued in New Mexico Didn’t ‘Find’ Startups, It Built the Future, that the state’s R&D foundation includes Los Alamos, Sandia, Kirtland Air Force Base, the Air Force Research Laboratory, White Sands, Spaceport America, and a quantum computing pipeline that does not exist anywhere else in North America.

The flagship play in Albuquerque is Q Station, a collaboration hub described on its own site as a partnership focused on driving high-tech economic development and new business opportunities to New Mexico, with partners including the Air Force Research Lab, the City of Albuquerque, the New Mexico Trade Alliance, New Mexico Tech University, NewSpace New Mexico, and Global Ties Albuquerque, citing that, “We work together to push innovation faster, developing technology the future needs now. We do it through partnerships, networking and leveraging those around us on a daily basis.”

They just launched, an Energy Challenge.

Toni Balzano, vice president of communications and strategy for Q Station, told Hobbs News that the organization is “working across the globe with energy sector companies, start-ups and tech developers and is working to recruit 20 or so energy sector companies to bring to Lea County for a 90-day accelerator,” with the explicit goal of developing a long-term pipeline of energy. New Mexico also now sits inside the Stargate footprint; OpenAI confirmed that Doña Ana County, New Mexico is one of three new Stargate sites that, combined with potential expansion near the Abilene flagship, can deliver over 5.5 gigawatts of capacity. Add Sandia’s grid modernization research, the Permian basin spilling across the state line, and New Mexico Tech’s energy engineering pipeline, and you have a state that is producing energy, consuming energy, researching energy, and now incubating energy companies in the same square mileage.

“The state realized with a massive windfall from a large oil reserve that they found, [that] they were literally taking money from the ground, which is awesome, but like all physical reserves…that may eventually run out,” J2 Ventures co-founder Alexander Harstrick told Tectonic. “They had an opportunity…to be able to invest in the future of technology in a way that only New Mexico can take advantage of.”

ARIZONA IS THE HIGHEST-VOLUME CLEAN ENERGY DEPLOYMENT MARKET IN THE COUNTRY

Arizona is the part of this that gets misread most often by people on both coasts who treat it as a retirement state with a chip factory, despite being one of the leading bioscience cities in the country. The reality is that Arizona has become the highest-volume clean energy deployment market in the Southwest. The Arizona Technology Council reported that Arizona saw more than $8 billion in clean energy investments in the 12 months between August 2022 and August 2023, among the highest in the nation, and that the state is now second in net generation of solar energy in the U.S., with 78 solar manufacturers operating in the state.

The infrastructure scale is not theoretical, and we need to recognize that it’s not just possible, it’s happening. The Papago Storage facility has developed the largest grid-scale battery in Arizona, the first of three Recurrent Energy projects. Ørsted and SRP brought online an 11 Mile Solar Center PV-plus-storage system, supplying among many things, Meta and its data center.

Arizona’s advantage is that it has hyperscale demand (TSMC, Meta, Microsoft, Apple, Intel), it has 300 days of sun, and it has utility regulators who, while imperfect, have moved faster on storage interconnection than most of the country.

What Arizona has not yet built, and where the startup ecosystem opportunity actually lives, is a venture studio infrastructure to spin out grid software, optimization tools, advanced cooling, transmission analytics, and the operational technology layer that energy companies are paying real money for right now.

TEXAS IS THE LARGEST OPPORTUNITY AND THE LARGEST PARADOX

Texas is, in the regional context, both the largest opportunity and a paradox. The on-the-ground reality of Abilene’s transformation, the Big Country was an attractive location for the inaugural Stargate installation because of its plentiful energy resources (including wind and solar farms), and yes, it’s noted that the state could face a power shortage of 40 gigawatts, equivalent to roughly half of the state’s current capacity.

The energy side, in particular, of the Texas ecosystem maps most cleanly through regions I have written about individually; Houston as the petrochemical and energy-grade engineering capital, the Permian as the hydrocarbon volume basin, West Texas as the wind and solar generation belt, the Hill Country hold our future in water, and Abilene as what Michael Bob Starr accurately described in an interview as “the funnel” connecting AI data center demand to nuclear, wind, solar, and natural gas supply. Abilene’s combination of Dyess Air Force Base, a contrarian small-town founder culture, and proximity to West Texas energy infrastructure made it strategically poised for an ecosystem play before Stargate ever got announced.

What is now happening on the ground confirms it; Starr is launching Paradox Labs, a venture studio focused on advanced energy, “With all the new initiatives and projects going in, including the Fermi nuclear power project in Amarillo, Abilene is the funnel to get to all that activity. With the addition of data centers, we’ve added new energy consumers alongside large energy producers. That’s the kind of environment that promotes innovative activity,” A venture studio partner JT Benton, co-founder of 9point8 Collective, made the point even more clear that, “Here we sit in this energy hotbed, where AI data centers and available scale will bring parts of the value chain here. That changes the game. It changes the capitalization of a place and reshuffles where value can be built.” Building credibility with industry decision-makers is, according to advisor Stan McHann, the part most founders fumble, and they’re not; “this has to be part of the solution for them, not just something they’re buying because it’s an AI product. It has to solve a real engineering problem, an operational problem, or a financial problem, or they won’t listen.”

The Austin layer of the energy story is also more developed than most realize. Falcon Energy Ventures, is a “A Grid Resilience Venture Studio Securing Today’s Grid. Powering Tomorrow’s Energy Ecosystem,” and the portfolio gives a useful picture of what an actual energy-focused venture studio is building right now: LLAP LLC (Energy Land for Solar and BESS), SolarSynapse (In-Panel IoT), SGDT (Smart Grid Distribution Transformer), Energy Semiconductor (next gen silicon thermal management), NexBreak (safer programmable electric breaker box), Battery Sentinel (smart automotive battery), Dyna-Factor (dynamic power factor correction), DCGrid.com (DC Transmission and Energy Super Highway), and Falcon Green Energy (solar, battery, and geothermal generation). That is what a sector-specialized venture studio portfolio actually looks like; nine ventures across generation, transmission, storage, and grid-edge hardware and software, designed to be capital efficient and operationally integrated rather than a scattershot collection of pitch decks. Texas has the demand, the basin, the universities, the defense and aerospace infrastructure, and now two operating energy-focused venture studios.

What Texas does not yet have is the regional connective tissue to other states; we’re working on this.

OKLAHOMA IS RUNNING THE MOST DISCIPLINED ECOSYSTEM BUILD IN THE REGION

Chronically underestimated but where founders, increasingly, are recognizing as one of the most disciplined ecosystem builds in North America.

Tulsa, in particular, is a model for what sector-specialized ecosystem building should look like. VentureBeat reported that since its launch in 2022, Rose Rock Bridge has accelerated 33 companies, initiated 22 active pilots with industry partners, and secured 11 customer contracts, resulting in over $50 million in funding raised by its member companies, with energy industry partners including Williams, ONEOK, Devon Energy, and Helmerich and Payne. That is not innovation theater; that is sector-aligned procurement-driven ecosystem building, exactly the kind of mechanism argued for in From Texas to Tulsa: How Innovation Shifts to Opportunity and in The Hidden Architecture of Startup Cities.

Oklahoma is also doing the hard policy work; the Oklahoman reported that a recently completed nuclear energy study sent to Oklahoma’s legislature and governor provides 350 pages of considerations to help determine if and how the state should pursue nuclear power as part of its energy portfolio, conducted through the Oklahoma Corporation Commission’s partnership with the Hamm Institute for American Energy. Tulsa already runs the heritage infrastructure of an energy capital, and OG&E’s renewables expansion across the Oklahoma-Arkansas footprint is extending that legacy into a renewables and storage capability.

ARKANSAS IS THE UNDERCOVERED PIECE OF THIS PICTURE

Arkansas is the most undercovered piece of this, which is the same observation I made in The Startup Frontier Hidden in America’s Supply Chain about Bentonville and the Northwest Arkansas corridor.

The energy build-out here is just as serious. Entergy Arkansas’s commitment to build the Ironwood Power Station, a natural gas-fired facility in Hot Spring County, with commercial operation expected in 2028 and 600 MW of solar power along with 350 MW of battery energy storage at the Arkansas Cypress facility, shows forward-thinking intention. The Arkansas Nuclear One power plant began commercial operation in 1974, with Unit 2 coming online in 1980, gives Arkansas an operational nuclear most states would now kill for. Southwestern Electric Power Company (SWEPCO)’s North Central Wind acquisition pulls Oklahoma wind into the Arkansas resource mix, and Walmart’s Bentonville HQ build-out is dragging supply chain decarbonization decisions into the same market.

Arkansas does not have a famous energy play yet; that is the gap, and it is one of the most interesting white-space openings in North American ecosystem building.

One Continuous Southwest Energy Belt

Tie these five states together and you have one continuous Southwest Energy Belt; New Mexico (quantum, directed energy, nuclear research, AI data centers), Arizona (solar generation, hyperscale-driven deployment, semiconductor demand), Texas (oil, gas, wind, solar, nuclear, AI infrastructure, refining, petrochemical engineering), Oklahoma (energy heritage, wind, nuclear study, energy tech incubation in Tulsa), and Arkansas (nuclear baseload, gas, wind purchased from Oklahoma, the Walmart-driven supply chain layer).

Stargate already crosses two of these state lines.

The wind farms operating in Oklahoma already deliver power to Arkansas customers.

The Permian crosses Texas and New Mexico without acknowledging either.

The AI data center load that Texas cannot fully absorb is now being placed in New Mexico and elsewhere across the region.

The capital, the talent, the workforce, and the procurement opportunities are already moving across state borders, and the only thing missing is the institutional infrastructure to coordinate it as one ecosystem rather than five competing economic development pitches.

How? Venture Studios, aligned, Are the Right Answer Here

The venture studio model becomes the right answer here but so new, it’s one that virtually no state has yet committed to with real money. Read, Your City’s Better Startup Plan: Invest in Venture Studios and Building a Tough Tech Venture Studio; the venture studio is uniquely suited to deep-sector, hard-tech, capital-intensive industries that accelerators were never designed to serve well. Matthew Burris, one of the leading authorities on the venture builder model, has been clear about the economics: “The venture studio model has produced some of the most promising companies of the last decade, with net IRRs that make traditional VC look soft. 60% Average net IRR is a slap across the face to VC’s ~30% top quartile returns.”

Trade associations or economic development zones help in this regard, but neither is ideally suited to the unique nature of the startup sector and our entrepreneurs. Most places add an accelerator or two, running founders through twelve weeks of pitch training and customer discovery; that is sometimes useful when founders already exist and need compression toward capital.

A venture studio actually builds the company from scratch, hires the founding team, originates the IP, and stays operationally embedded until product-market fit.

In an industry where the technical problem is “design a smart distribution transformer that survives a Texas summer,” the accelerator model is not even an option. Falcon Energy Ventures, Paradox Labs, and the energy programming inside Q Station, Rose Rock Bridge, and the Arrowhead Center are all converging on the same conclusion from different starting points. Which is what we want to have happen because as covered in Putting a Bow on your Startup Ecosystem, the venture studio sits at the productive end of the ecosystem bow; the place where capital, talent, and operations are combined under one roof to spin out companies that wouldn’t have existed otherwise. It fixes (or could fix) what universities and accelerators fail to deliver while associations and development zones simply don’t serve startups.

The collaboration I want to see, and the one I think the region’s economic development professionals, sovereign wealth funds, state investment offices, and energy industry corporate venture arms should be building right now, is a coordinated Southwest Energy Venture Studio Network. Studios, in every appropriate major city, each with its own sectoral focus (advanced energy in Abilene/Texas, grid resilience in Austin/Texas, directed energy and quantum infrastructure in New Mexico, solar manufacturing in Arizona, energy tech and nuclear in Oklahoma, supply chain and nuclear in Arkansas), sharing domain expertise, sharing deal flow, sharing portfolio company introductions, sharing technical talent, and sharing customer access to the utilities, data centers, defense agencies, and oil and gas majors that span the region.

Alongside that network, an incubator layer running in parallel; not the standard accelerator-as-marketing-program, but a genuine founder development environment that takes engineers, military veterans transitioning out of Dyess, Holloman, Kirtland, Tinker, and Little Rock Air Force Bases, energy industry operators, and university researchers, and brings them into the funnel as capable entrepreneurs before a venture studio ever needs them. The incubator builds the founders; the venture studios build the companies; the regional capital pool and the existing energy corporates buy and pilot the products.

We know Why Startup Ecosystems Fail at Scale and Why Venture Capital Avoids your Startup Ecosystem; the real failure of most regional ecosystem efforts is not lack of capital or lack of programs; it is lack of experience, connection, and capacity to take a founder from idea to credible company. A venture studio network spanning five states fixes capacity by sharing it. It also fixes the “cargo-cult” problem I describe at length in the book, where regions copy Silicon Valley’s surface features and never build the underlying structural conditions. The Southwest does not need to be Silicon Valley. It needs to be the place where the next generation of energy companies actually get built, by founders who already know the difference between a transformer and a transmission line.

If you are an economic development director in Albuquerque, Phoenix, Tucson, Tulsa, Oklahoma City, Houston, Midland, Amarillo, Abilene, Little Rock, or Fayetteville, what I hope you ask this week is why we’re not connecting your excellence in energy, to better serve innovation and entrepreneurship. If you are an investor, the question is whether your deal flow is reaching the founders who are actually in the basins, the substations, the labs, and the bases, or whether your pipeline still routes through the same five demo days everyone else funds in their city.

In hard tech, you’ll often find yourself stuck because your home ecosystem treats you like a square peg, wherein IP, deep tech, hardware, or infrastructure, should meet the same expectations as a Lean Startup. That’s not possible, the resources you need aren’t found sufficient locally, they’re in the region.